7 Boring Habits That Turned My $48k Into $632k (No Get-Rich-Quick)

Tobiloba OdejinmiBy Tobiloba Odejinmi

Education

May 31, 2026 • 3:21 PM

2m2 min read

Verified

The Core Insight

Anthony O'Neal outlines seven foundational habits that transformed his financial life from living in his car to building a seven-figure business. The core argument is that wealth is not built through complex schemes, but through boring, consistent habits: automating savings, aligning spending with values, conducting monthly money dates, investing early, tracking every dollar, investing in personal skills, and practicing intentional generosity.

T

Education Specialist & Editor

Tobiloba Odejinmi

Tobiloba Odejinmi is an education specialist dedicated to helping students and lifelong learners discover the best scholarship opportunities, study techniques, and career pathways.

The Kodawire Editorial Team consists of experienced journalists and subject matter experts dedicated to delivering accurate, well-researched, and engaging content.

The Truth About Building Wealth: It’s Not Sexy, It’s Simple

The Bottom Line

Automate Everything: Move your savings to a High-Yield Savings Account (HYSA) immediately to stop "donating" interest to traditional banks.

The 12-15% Rule: Prioritize investing 12-15% of your income into index funds or 401(k)s before you pay your bills.

Conduct a Legacy Check: Audit your last three months of bank statements to ensure your spending aligns with your stated values, not just convenience.

Track Your Leaks: Spend seven days recording every single penny to identify "spending leaks" like daily vending machine runs or unused subscriptions.

There is a persistent myth that building wealth requires a finance degree, a six-figure salary, or access to some clandestine investment formula. I have spent years digging into the mechanics of personal finance, and I can tell you with certainty: the barrier to entry isn't a lack of income. It is a lack of alignment. When I look at the data, the difference between those who struggle and those who build a net worth of seven figures often comes down to seven boring, unsexy, and highly effective habits. If you are looking to master your money, understanding how the 1% actually manage their money is the first step toward true independence.

If you are feeling overwhelmed, you are not alone. Nearly one in four Americans currently has zero emergency savings, and four in ten have absolutely no exposure to the stock market. The top 10% of the population owns 90% of all stocks, not because they have a secret, but because they have a system. Consistency is the engine of wealth. Consider this: if you invest just $100 a month for 40 years at a 10% return, you contribute $48,000 of your own money, but you end up with approximately $632,000. That is $584,000 in interest, a 1,200% return on your contributions. That is the power of time and discipline.

The 7 Boring Habits That Build Millionaires

Building wealth is not about timing the market or chasing the next "get rich quick" scheme. It is about the mundane, daily decisions that compound over decades. For those starting from scratch, reclaiming your financial future is entirely possible with these foundational shifts.

Consistent financial management is the key to long-term wealth. (Credit: Leeloo The First via Pexels)

Why You Can Trust This

My approach to this analysis is rooted in independent research and the observation of long-term financial principles. I have vetted these habits against standard economic data and the experiences of those who have successfully transitioned from financial instability to long-term wealth. I do not rely on "get rich quick" hype; instead, I focus on the mathematical reality of compounding interest and the psychological necessity of behavioral change.

Automate Your Savings: Discipline is faith in action. By setting up an automatic transfer to a High-Yield Savings Account (HYSA), you remove the temptation to spend. Traditional banks often pay pennies in interest, while an HYSA allows your emergency fund to actually grow.

Align Spending with Values: Perform a "legacy check." Pull your bank statements from the last three months. If your top values are family and education, but your statements show heavy spending on takeout and streaming services, you have a misalignment. Your money should move toward your purpose, not away from it.

The Monthly Money Date: Block 30 minutes every month to sit down with your statements. Whether you are single or married, you cannot build wealth if you do not know where your money is going. Use this time to set one specific financial focus for the month ahead.

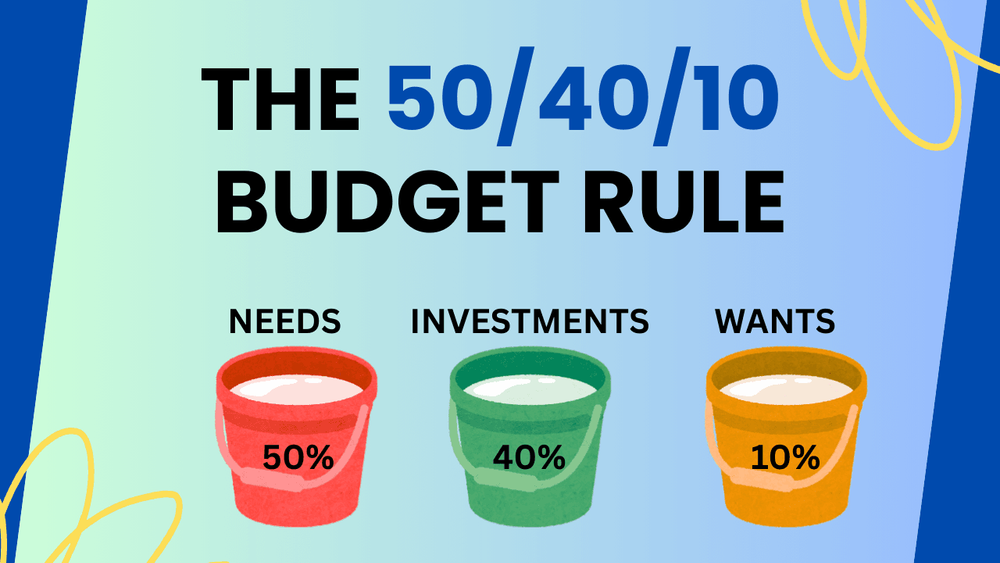

Invest Before You Spend: Adopt the "pay yourself first" rule. Before the bills hit, move 12-15% of your income into index funds or a 401(k). This ensures your future is funded before your current lifestyle consumes your resources.

Track Every Dollar: For seven days, record every single penny. This is not about judgment; it is about awareness. You will likely find "leaks", small, habitual purchases that, when added up, represent a significant portion of your potential investment capital.

Invest in Your #1 Asset: Your mind is your greatest wealth-building tool. Spend money on books, courses, and skill-building workshops. Unlike material goods, skills pay dividends for the rest of your life.

The Multiplier Effect: Generosity, including tithing, creates a mindset of stewardship. It shifts your focus from scarcity to abundance and positions you to manage resources with greater wisdom and favor.

Tracking your expenses is a critical step in identifying spending leaks. (Credit: Pavel Danilyuk via Pexels)

The Real ROI

From a strategic standpoint, the return on investment for these habits is massive. When you move money from a traditional savings account to an HYSA, you are capturing "free" yield that would otherwise be lost to bank margins. When you invest in skills, you are increasing your human capital, which is the only asset that can consistently outpace inflation. In 2026, with economic volatility remaining a constant, the "ROI" of having a liquid emergency fund and a consistent investment strategy is the difference between surviving a market dip and thriving through it.

Analytical Value-Add: Why Most People Fail at Wealth Building

The primary reason most people fail is "lifestyle creep." As income rises, spending rises to match it, leaving no margin for wealth creation. Furthermore, many people treat their cash as "lazy money," leaving it in accounts that lose value against inflation. True wealth is not defined by a high income; it is defined by the margin between what you earn and what you spend. If you earn $200,000 but spend $200,000, you are not wealthy, you are just expensive to maintain. For those looking to optimize their tax efficiency while building this margin, understanding tax-saving strategies is essential.

The Other Side of the Story

Many financial influencers will tell you that you need to "hustle" and work 80-hour weeks to build wealth. I disagree. The most sustainable wealth is built through boring, automated, and consistent habits. You do not need to burn yourself out to become a millionaire; you need to be consistent enough to let time and compound interest do the heavy lifting for you.

The Execution Strategy

To implement this, managers and individuals should treat their personal finances like a corporate P&L.

Audit: Identify your "fixed costs" versus "discretionary leaks."

Automate: Use banking software to schedule transfers on the day your paycheck hits.

Review: Treat your Monthly Money Date as a non-negotiable board meeting with yourself.

Modern banking tools make it easier than ever to automate your savings. (Credit: Liza Summer via Pexels)

The Decision Matrix

Not sure where to start? Use this simple guide:

If you have...

Your first step is...

No emergency fund

Open an HYSA and automate $5/week.

Debt but no investments

Track spending for 7 days to find $50/month to redirect.

Basic savings

Open a brokerage account and set up a recurring S&P 500 index fund purchase.

The Absolute Best Case

If you start today, the best-case scenario is not just a high net worth. It is the acquisition of "margin." Margin gives you the freedom to choose your work, the ability to weather a job loss without panic, and the capacity to be generous when others are in need. By 2030, the person who started today will be in a fundamentally different position than the person who waited for the "perfect time."

High-Yield Savings: Look for FDIC-insured accounts that offer competitive APY (Annual Percentage Yield) compared to traditional national banks.

Brokerage Platforms: Utilize low-cost, user-friendly platforms that allow for fractional shares and automated recurring investments into broad-market index funds.

Skill Development: Prioritize platforms that offer verified, substance-heavy courses in your specific industry or in emerging technologies like AI automation.

What Do You Think?

We have covered a lot of ground, from the math of compounding interest to the psychological shift required to prioritize your future self. I am curious about your perspective: If you had to pick just one of these seven habits to master in the next 30 days, which one would have the biggest impact on your life? I will be in the comments for the next 24 hours to hear your thoughts and answer your questions.

Traditional banks often pay negligible interest, whereas a High-Yield Savings Account (HYSA) allows your emergency fund to grow significantly more over time, helping you keep pace with inflation.

It is the practice of moving 12-15% of your income into investments like index funds or a 401(k) before paying any other bills, ensuring your future is funded before your current lifestyle consumes your resources.

The article recommends tracking every single penny you spend for seven days. This process creates awareness and helps you identify small, habitual purchases that add up to significant amounts of lost investment capital.

Active Engagement

Was this information helpful?

Join Discussions

0 Thoughts

Editorial Team • Question of the Day

"What is the one "spending leak" you discovered after tracking your expenses for a week?"